Franchising has long been one of the most powerful models in business ownership. The systems are proven, the branding is established, and the operational playbook already exists. But even with a strong franchise concept, one challenge consistently separates operators who grow from those who struggle: access to capital.

Whether you are opening your first location, acquiring an existing franchise, refinancing expensive debt, remodeling a store, or scaling to multiple units, financing is often the deciding factor between stalled growth and sustainable expansion.

In today’s market, franchise financing has become both more competitive and more specialized. Lenders are no longer looking only at credit scores and tax returns. They are evaluating brand strength, unit economics, operator experience, cash flow trends, territory growth potential, and industry performance in real time.

For franchisees, understanding how financing actually works, and how lenders evaluate opportunities, can create a major competitive advantage.

Why Franchise Businesses Are Attractive to Lenders

Compared to many independent startups, franchises often present lower perceived risk to lenders because they operate within an established system. Strong franchises typically provide:

- Recognizable branding

- Proven operating procedures

- Historical performance data

- Existing customer demand

- Franchise support systems

- Easier benchmarking against similar locations

From a lender’s perspective, a franchise with consistent unit-level performance is often easier to underwrite than a completely independent concept with no operating history.

However, not all franchises are viewed equally.

A nationally recognized quick-service restaurant brand with hundreds of profitable units may receive dramatically different financing terms than a newer franchise concept with limited operating history. The strength of the franchisor matters. The operator matters even more.

At the end of the day, lenders want to answer one core question:

Can this business consistently generate enough cash flow to comfortably repay the debt while still allowing the operator to succeed?

The Main Types of Franchise Financing

Franchise financing is not one-size-fits-all. Different stages of growth require different lending structures.

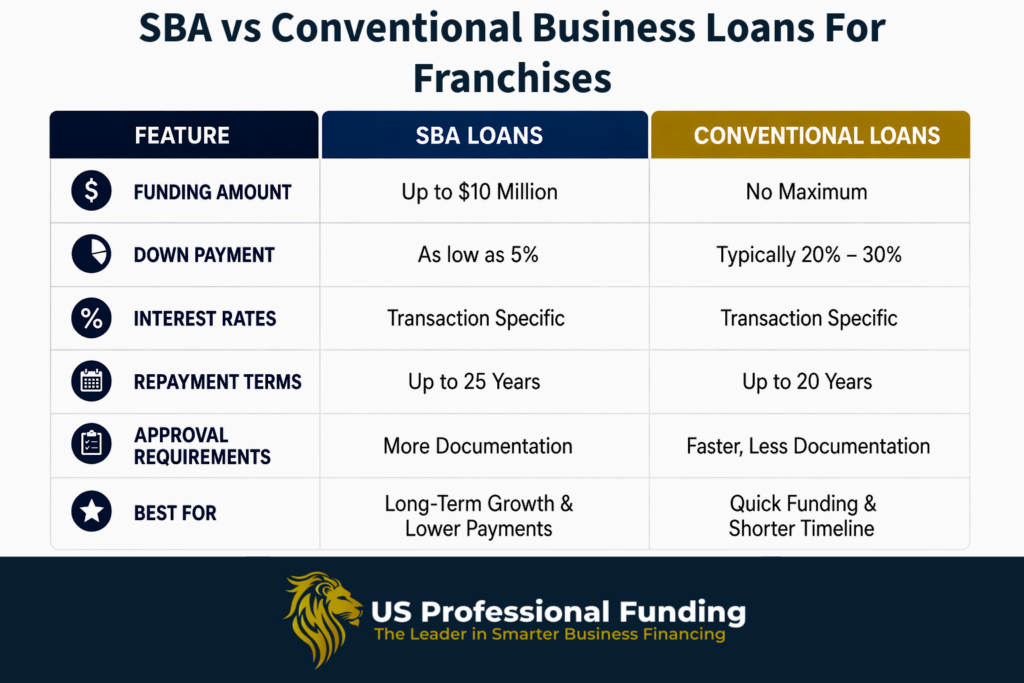

SBA Loans

SBA financing remains one of the most common solutions for franchise acquisitions, startups, and expansions.

These loans are partially guaranteed by the government, which reduces lender risk and often allows for:

- Longer repayment terms

- Lower down payments

- Competitive interest rates

- Higher leverage

SBA loans are commonly used for:

- Buying an existing franchise

- Opening a new location

- Partner buyouts

- Equipment purchases

- Working capital

- Real estate acquisitions tied to the business

For qualified operators, SBA financing can be one of the most efficient forms of long-term capital available.

That said, approval is rarely quick or automatic.

Lenders still scrutinize:

- Personal credit

- Liquidity

- Industry experience

- Debt-to-income ratios

- Existing obligations

- Historical business performance

- Franchise brand strength

A strong borrower with a weak concept may still struggle to secure financing. Likewise, a strong franchise brand does not automatically offset weak financials or poor management history.

Conventional Bank Financing

Traditional bank financing is often available for established franchisees with strong cash flow and healthy balance sheets.

Banks tend to prefer:

- Multi-unit operators

- Established locations

- Consistent profitability

- Significant liquidity

- Strong debt-service coverage

For experienced franchisees expanding into additional units, conventional financing can sometimes provide more favorable pricing than SBA loans.

However, banks are typically more conservative with startups or first-time operators.

Equipment Financing

Many franchise concepts require substantial equipment investments upfront.

Restaurants, fitness franchises, laundromats, medical concepts, automotive franchises, and hospitality operators can easily spend hundreds of thousands, or even millions, on equipment alone.

Equipment financing allows operators to spread those costs over time rather than deploying all available capital upfront.

This can improve liquidity during the critical early stages of operations when cash flow is still stabilizing.

In many cases, the equipment itself serves as collateral, which can simplify approvals compared to unsecured lending.

Franchise Startup Financing

Opening a new franchise location is very different from acquiring an existing profitable store.

With a startup, lenders are underwriting projected performance rather than existing cash flow.

That means the emphasis shifts heavily toward:

- Franchise brand strength

- Operator experience

- Liquidity reserves

- Market demographics

- Business plan quality

- Franchise Disclosure Document (FDD) analysis

One mistake many new franchisees make is underestimating how much working capital they actually need.

Buildout delays, slower ramp-up periods, labor shortages, inventory costs, and seasonal fluctuations can create significant pressure during the first 12 months.

The operators who survive and thrive are usually the ones who capitalize properly from the beginning, not necessarily the ones who start with the smallest investment.

Multi-Unit Expansion Financing

Some of the strongest franchise operators grow aggressively by leveraging financing strategically.

Once an operator has demonstrated successful execution at one or more locations, lenders often become significantly more flexible.

Experienced multi-unit franchisees may qualify for:

- Larger credit facilities

- Development lines

- Expansion capital

- Refinance opportunities

- Real estate-backed financing

- Portfolio lending structures

At this level, lenders are often evaluating the operator more than the individual location.

Strong systems, management infrastructure, reporting accuracy, labor controls, and operational consistency become critical.

The transition from owner-operator to scalable enterprise is where many franchise businesses either plateau or accelerate dramatically.

What Lenders Really Look For

Many franchisees assume financing decisions are based mostly on credit scores.

In reality, sophisticated lenders evaluate the entire picture.

Some of the biggest approval factors include:

Cash Flow

Cash flow is king in commercial lending.

Lenders want to see whether the business generates enough income to comfortably cover debt obligations while still leaving room for operational stability.

Consistent profitability matters far more than flashy revenue numbers.

Liquidity

Having reserves matters.

Even profitable operators can face temporary setbacks:

- Equipment failures

- Construction delays

- Economic slowdowns

- Labor issues

- Seasonality

Liquidity provides stability and gives lenders confidence that the borrower can weather challenges.

Operator Experience

Experience matters enormously in franchising.

An experienced operator with a track record of successful execution will almost always receive stronger consideration than a first-time business owner entering a highly competitive industry.

Brand Performance

Some franchise systems simply perform better than others.

Lenders often analyze:

- Historical franchise closure rates

- Average unit volumes

- Litigation history

- Corporate support quality

- Franchisee profitability

- Market saturation risks

Strong concepts with healthy unit economics are substantially easier to finance.

Common Financing Mistakes Franchisees Make

Underestimating Total Project Costs

Many operators budget only for franchise fees and construction while overlooking:

- Working capital

- Payroll ramp-up

- Marketing

- Inventory

- Delays

- Contingencies

Insufficient capitalization is one of the most common causes of early operational stress.

Waiting Too Long to Explore Financing

Many franchisees begin looking for financing only after signing agreements or committing deposits.

The strongest financing outcomes usually happen when operators prepare early and structure projects strategically before commitments are finalized.

Focusing Only on Interest Rates

The cheapest money is not always the best money.

Loan structure, repayment flexibility, prepayment penalties, collateral requirements, amortization periods, and lender experience can all impact long-term success.

A financing structure that preserves liquidity and operational flexibility can be far more valuable than simply chasing the lowest rate.

The Franchise Landscape Is Still Growing

Despite economic uncertainty, franchising continues to attract entrepreneurs, investors, and multi-unit operators across industries ranging from restaurants and fitness to healthcare, home services, automotive, hospitality, and retail.

Many lenders remain highly active in the franchise sector because well-run franchise businesses can produce stable, scalable cash flow over long periods of time.

The operators positioned best for growth are typically the ones who:

- Understand their numbers

- Maintain strong financial discipline

- Preserve liquidity

- Choose scalable concepts carefully

- Build relationships with experienced lenders early

Financing is not just about securing capital. It is about creating a structure that allows the business to grow sustainably without creating unnecessary operational pressure.

For franchisees looking to expand in today’s market, strategic financing may ultimately become one of the most important growth tools they have.

Christopher Cornella is the Vice President of Business Development at US Medical Funding and US Professional Funding, where he specializes in commercial financing solutions for healthcare practices, medical spas, restaurants, franchises, and small businesses nationwide. He works closely with business owners on startup financing, acquisitions, expansion capital, equipment financing, SBA & Conventional lending and operational growth strategies. Through his industry insight and experience structuring financing across multiple sectors.